When most people in the UK think about saving, they picture putting money into a Cash ISA or a regular savings account. But for those who want their money to grow faster, a Stocks and Shares ISA can be a powerful tool. This guide explains what it is, how it works, the pros and cons, and whether it might be right for you.

What Is a Stocks and Shares ISA?

A Stocks and Shares ISA (sometimes called an “investment ISA”) is a tax-efficient investment account available to UK residents.

Instead of earning interest like a savings account, the money you put in is invested in assets such as:

- Company shares (equities)

- Corporate or government bonds

- Investment funds (unit trusts, OEICs, index funds)

- Exchange-Traded Funds (ETFs)

- Investment trusts

Any returns you make inside a Stocks and Shares ISA — whether from dividends, capital gains, or interest — are completely tax-free.

The £20,000 Annual Allowance

Every UK adult has an annual ISA allowance of £20,000 for the 2025/26 tax year.

This allowance is shared across all ISA types — Cash ISAs, Stocks and Shares ISAs, Innovative Finance ISAs, and Lifetime ISAs.

For example:

If you put £5,000 into a Cash ISA, you still have £15,000 left to invest in a Stocks and Shares ISA during the same tax year.

This flexibility allows you to split your allowance across different ISAs depending on your goals.

Why Invest Through a Stocks and Shares ISA?

1. Tax-Free Growth

Normally, when you sell investments at a profit, you might pay Capital Gains Tax (CGT) once gains exceed the annual allowance (£3,000 in 2025/26).

Dividends above £500 (from April 2025) are also taxable.

Inside a Stocks and Shares ISA:

- No CGT on investment growth

- No dividend tax on payouts

- No income tax on bond interest

2. Compound Growth Over Time

Even small, regular contributions can grow significantly over time thanks to compound growth. Starting early lets you take full advantage of tax-free returns over decades.

3. Flexibility

You can invest in a wide range of assets — from low-risk government bonds to higher-risk global shares — depending on your comfort level and goals.

Risks You Need to Know

Unlike a Cash ISA, your capital is not guaranteed. Investment values can fall as well as rise, and you may get back less than you invest.

However, over the long term, history shows that stocks and shares tend to outperform cash savings, particularly after accounting for inflation.

Stocks and Shares ISA vs Cash ISA

| Feature | Stocks & Shares ISA | Cash ISA |

|---|---|---|

| Returns | Variable (can be higher but not guaranteed) | Fixed or variable, usually lower |

| Risk | Medium to high | Very low (FSCS protected up to £85k per provider) |

| Best for | Long-term growth (5+ years) | Short-term savings and emergency funds |

| Tax benefits | No CGT, no dividend tax, no income tax | Interest tax-free |

| Access | Withdraw anytime (but may affect growth) | Withdraw anytime |

Why It’s Worth Starting Early

Some people hesitate, thinking they don’t have enough money to invest. But even small investments add up.

- Future-proofing: Building contributions early makes use of tax-free growth before your income or savings rise.

- Use it or lose it: ISA allowances don’t roll over. Skipping a year means losing that year’s £20,000 tax shelter permanently.

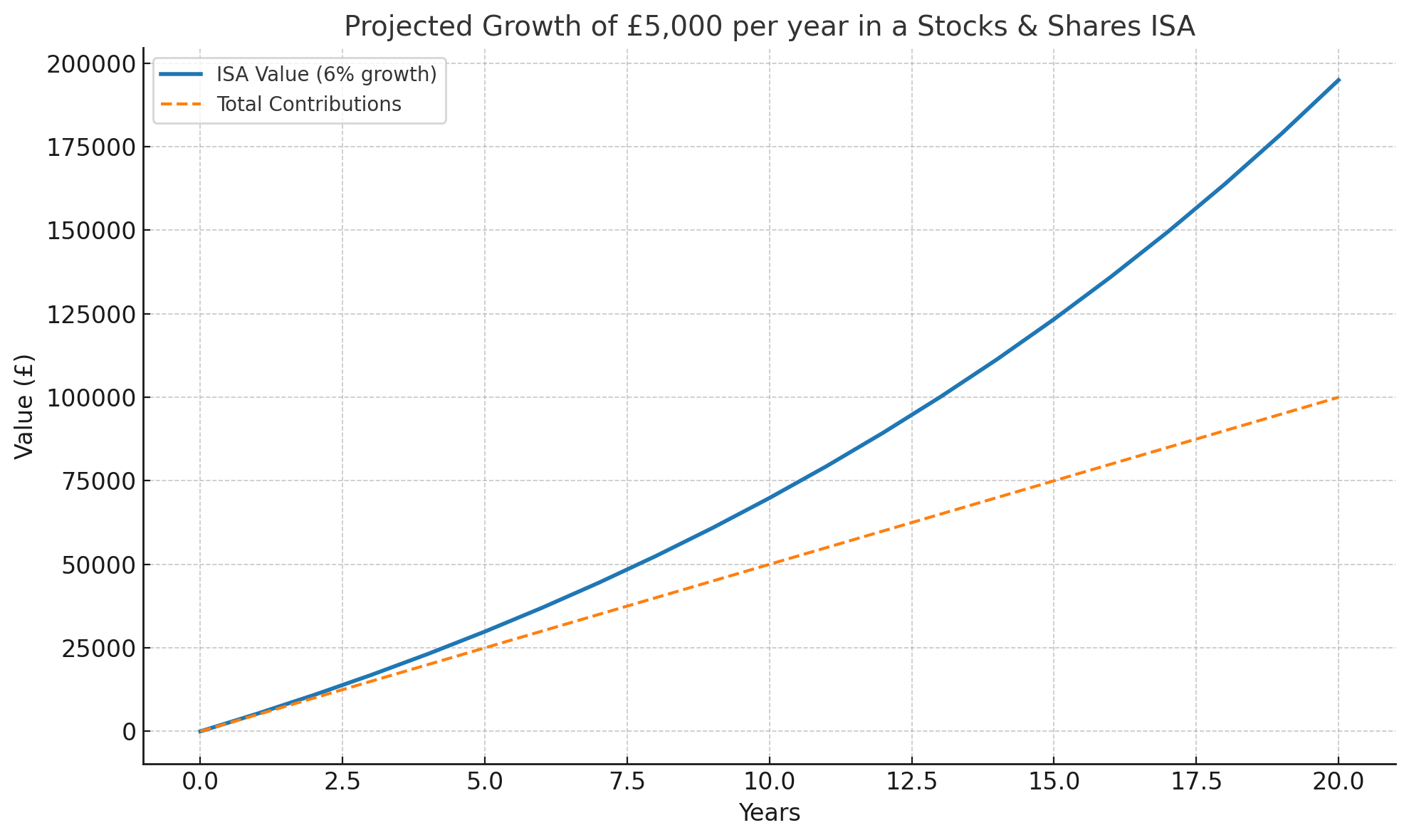

Example of Potential Growth

If you invest £5,000 per year in a Stocks and Shares ISA for 20 years with an average 6% annual return:

- Total invested: £100,000

- Value after 20 years: roughly £184,000

- Entirely tax-free

Outside an ISA, some of this gain could be lost to CGT or dividend tax.

| Year | Contributions | Value (6% growth) |

|---|---|---|

| 5 | £25,000 | £29,000 |

| 10 | £50,000 | £67,000 |

| 15 | £75,000 | £120,000 |

| 20 | £100,000 | £184,000 |

How to Open a Stocks and Shares ISA

1. Choose a Platform or Provider

You can open one through:

- Traditional banks

- Investment platforms such as Hargreaves Lansdown, AJ Bell, or Vanguard

- App-based providers like Moneybox, Freetrade, or Trading 212

2. Decide on Your Investment Approach

- Hands-off: Choose a ready-made portfolio or use a robo-advisor.

- Hands-on: Select individual funds, ETFs, or shares yourself.

3. Start Small and Build Up

Many providers allow regular investing from as little as £25 a month, making it accessible to almost anyone.

Who Should Consider a Stocks and Shares ISA?

- Younger savers looking to build wealth over decades

- Higher-rate taxpayers who benefit most from tax-free growth

- Anyone with long-term goals like retirement, education funding, or financial independence

Final Thoughts

A Stocks and Shares ISA is one of the most effective long-term wealth-building tools available to UK savers. It offers tax-free growth, flexibility, and the potential to outperform cash over time.

While there’s risk involved, the greater risk for many is leaving money in cash where inflation steadily erodes its value.

Start early, invest regularly, and think long term.

Explore our full range of Investment Tools and related guides, including What Is a Cash ISA? and UK Investing 101: What Is an ISA?