Budgeting has a reputation problem. Many people picture endless spreadsheets, strict penny-pinching, and rules that make life feel restrictive. But budgeting doesn’t have to be complicated or joyless. One of the simplest and most effective frameworks is the 50/30/20 rule — a practical guide that helps you balance spending, saving, and living well.

In this article, we’ll explain how the rule works, how it applies to UK households, and how you can adapt it to your lifestyle.

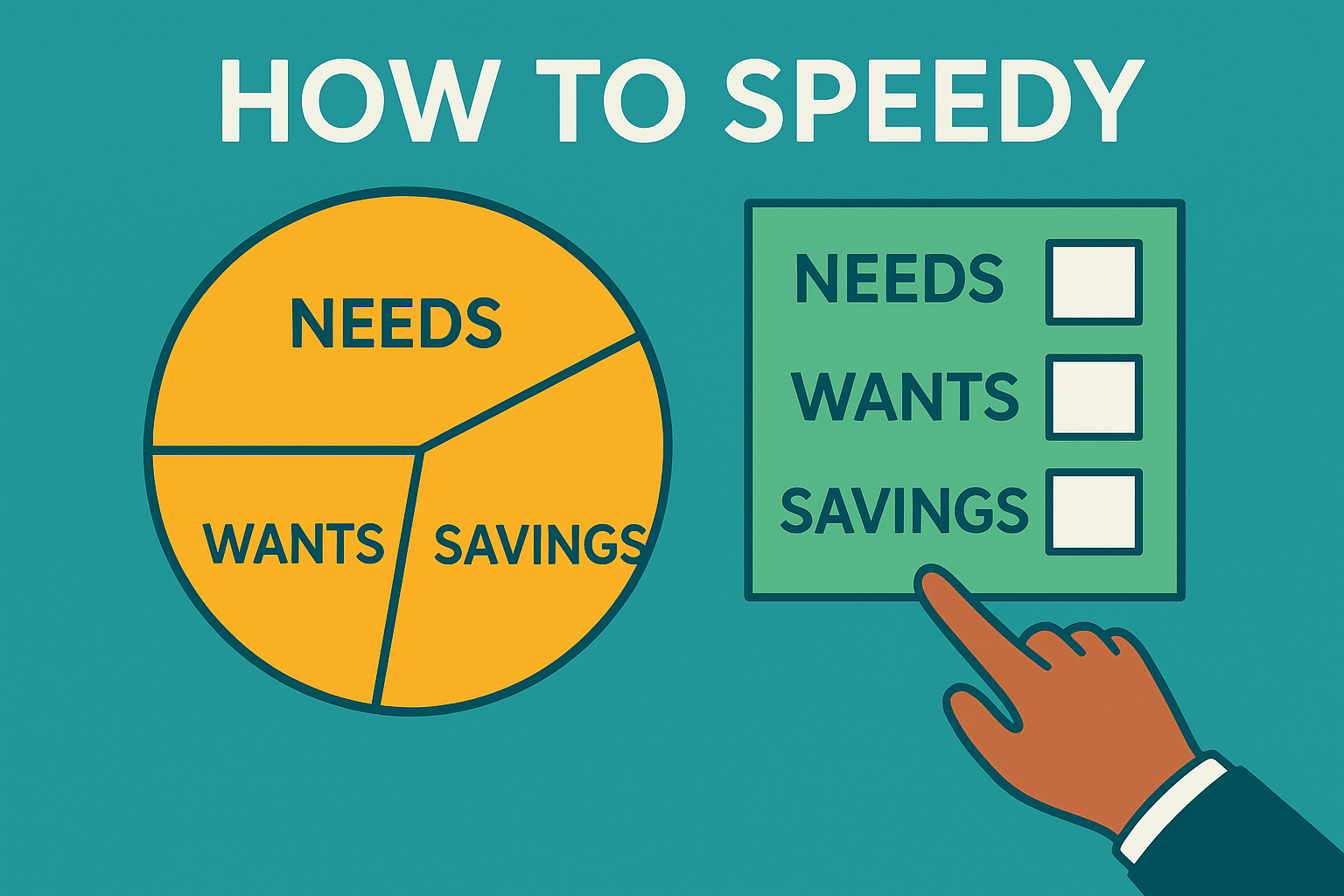

What Is the 50/30/20 Rule?

The 50/30/20 rule divides your after-tax income into three clear categories:

- 50% Needs – Essential living costs you can’t avoid

- 30% Wants – Lifestyle choices that make life enjoyable

- 20% Savings and Debt Repayment – Contributions that build financial security

This simple balance lets you cover essentials, enjoy life today, and save for tomorrow — without micromanaging every expense.

50%: Needs

Needs are the essentials that keep your household running day-to-day. For most UK families, this includes:

- Rent or mortgage payments

- Council tax

- Utilities (gas, electricity, water)

- Basic groceries

- Transport costs (fuel, public transport, insurance)

- Minimum debt repayments

In many parts of the UK — especially London — housing alone can easily take up 40–50% of take-home pay. Don’t worry if you can’t hit the 50% exactly; the rule is meant as a guideline, not a strict law.

If your housing costs push you over the limit, focus on keeping your “wants” lean until your finances rebalance.

30%: Wants

Wants are non-essential but add enjoyment and comfort to life. These might include:

- Eating out or takeaways

- Holidays and weekend trips

- Streaming services and subscriptions

- Shopping, hobbies, or leisure activities

- Nights out, concerts, or sporting events

It’s easy for “wants” to creep up unnoticed — especially with contactless payments and subscription renewals. Tracking them once a month helps you stay aware without giving everything up.

20%: Savings and Debt Repayment

This is the category that builds long-term financial freedom. In the UK, your 20% might include:

- Contributions to a Cash ISA or Stocks and Shares ISA

- Payments into a personal pension

- Building an Emergency Fund

- Extra repayments on credit cards, personal loans, or mortgages

This 20% is what moves you forward. Regular saving builds resilience and allows your money to compound over time — key if you want to escape the paycheck-to-paycheck cycle.

Example: The 50/30/20 Rule in Action

Let’s imagine a monthly take-home pay of £2,500:

| Category | % | Example Allocation |

|---|---|---|

| Needs | 50% (£1,250) | £800 rent, £150 council tax, £200 utilities, £100 transport |

| Wants | 30% (£750) | £250 dining out, £200 shopping, £150 holidays, £150 entertainment |

| Savings/Debt | 20% (£500) | £300 to ISA, £100 to emergency fund, £100 extra debt payments |

If your rent or bills take more than 50%, that’s fine — the key is to see the trade-offs clearly and make adjustments consciously.

Why the 50/30/20 Rule Works

- Simplicity: You don’t need to track every purchase — just keep broad categories in balance.

- Flexibility: It scales to any income level. Whether you earn £2,000 or £6,000 a month, the ratios work proportionally.

- Balance: You still enjoy life while staying on track financially.

It’s a realistic framework that prevents burnout while keeping savings a priority.

The Limitations in the UK

- High housing costs: Rent and mortgages in major cities often break the 50% “needs” target.

- Irregular income: Freelancers or gig workers may need to average their budgets over several months.

- Debt load: Households with high-interest debt may need to allocate more than 20% to repayments.

The rule is meant to be flexible — a starting point, not a fixed formula.

Adapting the Rule to Your Life

You can adjust the ratios to fit your reality:

- 60/20/20 if housing costs dominate

- 40/20/40 if you’re debt-free and want to save aggressively

Focus on progress, not perfection. Awareness of your spending patterns matters more than sticking to exact percentages.

How to Put It Into Practice

- Work out your take-home income

Use your payslip or HMRC’s online calculator to find your post-tax amount. - Categorise your spending

Review one to three months of statements and label each expense as a need, want, or saving. - Automate your savings

Set a standing order to move money into your ISA or savings account right after payday.

You can explore options in Pay Yourself First: The Easiest Way to Build Wealth in the UK. - Track your wants flexibly

Use digital banking tools (like Monzo or Starling) to set category budgets. - Review monthly

If you go off track, rebalance next month. Budgeting is about direction, not perfection.

Visualise Your 50/30/20 Budget

Use our Budgeting Tool to visualise your spending and savings breakdown — a simple way to see progress without spreadsheets.

Conclusion: A Framework, Not a Straightjacket

The 50/30/20 rule is about awareness and balance, not restriction. It’s one of the most practical budgeting systems for UK households — simple enough for beginners, flexible enough for life’s changes.

Combine it with smart habits like automating your savings, building your Emergency Fund, and using tax-efficient accounts such as ISAs. Over time, these small steps help you stay in control of your money and build lasting financial confidence.

See our full list of Investment Tools.